WIXOM, Mich. – RevSpring has once again demonstrated its leadership role in security, compliance, and ethics with the renewal of key security requirements for PCI DSS v3.1.

To comply with the latest version of PCI DSS, RevSpring performed upgrades to its governing policies and processing operations.

“Adhering to the highest levels of security and compliance protocols in the regulated space is RevSpring’s top priority,” said Peter David, RevSpring’s chief security officer. “We understand that serving our clients and meeting their changing expectations is paramount to reflecting our beliefs in transparency and ethics.”

RevSpring’s leadership and commitment is demonstrated each year by the investment of certifying its facilities nationwide using qualified, independent security experts. The PCI DSS audit was conducted by Solutionary.

Customers interested in receiving copies of the security reports should contact their sales representative or email learnmore@revspringinc.com.

About RevSpring

RevSpring’s core service offerings include data hygiene and analytics, secure document creation and delivery, multi-channel communications, electronic billing and archival services and online payment tools, all while ensuring compliance with regulatory guidelines. RevSpring holds multiple security certifications including PCI DSS Level 1, HIPAA/HITECH and SSAE 16 SOC 2 and maintains rigorous legislative and regulatory compliance programs. It serves a large and diverse customer base across the healthcare, receivables management, financial services, insurance, home services and other end-markets. Its family of companies includes Talksoft, Revenue Advantage, TECH LOCK and Healthcare Revenue Strategies. To learn more visit www.revspringinc.com.

Contact:

Heather Taylor

765.730.6632

htaylor@revspringinc.com

RevSpring Renews Critical Security Requirements, Complies with PCI DSS

http://www.insidearm.com/accelerate-revenue/revspring-renews-critical-security-requirements-complies-with-pci-dss/

http://www.insidearm.com/feed

insideARM

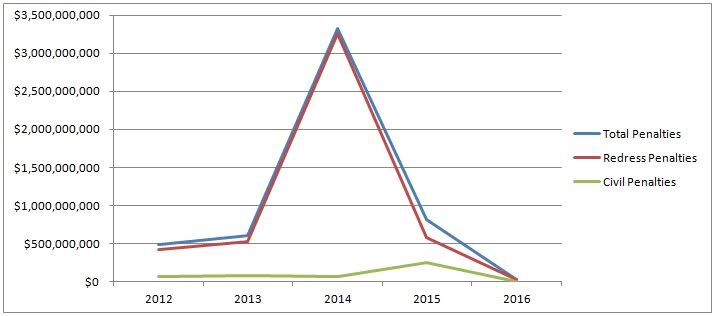

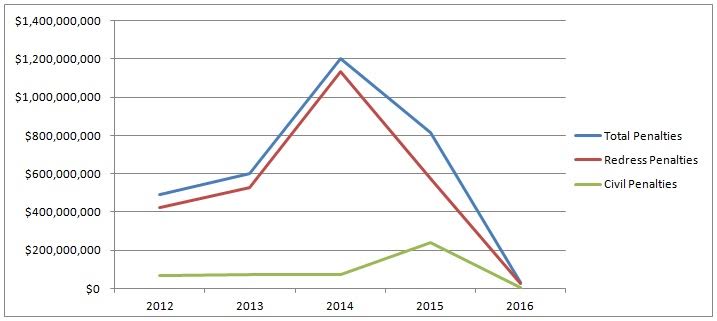

As you can see in the chart above, 2014 was a big year for the CFPB. The Bureau ended up issuing more than $3 billion in fines in 2014 alone, more than $2 billion of those penalties coming in

As you can see in the chart above, 2014 was a big year for the CFPB. The Bureau ended up issuing more than $3 billion in fines in 2014 alone, more than $2 billion of those penalties coming in  Types of Penalties

Types of Penalties