This article previously appeared on The Consumer Financial Services Blog and is re-published here with permission.

The U.S. District Court of the Western District of North Carolina recently stayed proceedings in a suit pending the U.S. Court of Appeals for the District of Columbia’s ruling on challenges to the Federal Communication Commission’s Declaratory Ruling and Order, 30 FCC Rcd. 7961 (2015) (the “FCC Order”) under the federal Telephone Consumer Protection Act (TCPA).

A copy of the opinion in Abplanalp v. United Collection Bureau, Inc. is available here.

The plaintiff’s credit card agreement contained an arbitration provision requiring that all claims against the lender, including claims against third parties to whom the plaintiff’s debt was assigned for collection, be subject to arbitration. The card issuer assigned the plaintiff’s account to a third party debt collector. The collector manually dialed the plaintiff’s phone from a telephone system that allegedly had the capacity to place an autodialed call.

The plaintiff filed suit in North Carolina state court against the collector alleging that the collector violated the TCPA by using an “automatic telephone dialing system” (ATDS) to contact her regarding the debt. Although the collector manually dialed the plaintiff’s phone, the plaintiff claimed that the collector’s telephone system had the capacity to place autodialed calls and was thus an ATDS.

The collector removed the case to federal court, and then moved to dismiss and compel arbitration. Alternatively, the collector moved to stay proceedings pending rulings in a consolidated appeal and a class action suit that could be dispositive of the plaintiff’s claims. The Court denied the collector’s motion to dismiss, but granted the collector’s motion to stay.

The Western District of North Carolina held that the plaintiff was not required to pursue her claims in arbitration because the arbitration provision in the card agreement was not binding. The Court disagreed with the collector’s assertion that the plaintiff consented to arbitration simply by using her credit card account. The Court noted that the arbitration provision was not dated, and contained neither the plaintiff’s signature nor a proof of notice. Furthermore, the arbitration provision did not contain information linking the agreement with the plaintiff’s account. Accordingly, the Western District of North Carolina denied the collector’s motion to dismiss and compel arbitration.

However, the Court granted the collector’s motion to stay proceedings pending resolution of the DC Circuit appeal of the FCC Order. The Court explained that several appeals of the FCC Order were consolidated by the United States Judicial Panel on Multidistrict Litigation before the Court of Appeals for the District of Columbia regarding challenges to the FCC Order defining telephone systems that qualify as an ATDS under the TCPA. The Court held that resolution of the consolidated appeals in the DC Circuit could be dispositive of the borrower’s TCPA claims, noting the lack of any rebuttal from the borrower regarding this issue.

Finally, the Court denied the collector’s motion to stay the proceedings pending final approval of the class action settlement in Graff v. United Collections Bureau, Inc., Case no. 2:12-cv-02402 (E.D.N.Y.). Although the borrower was a member of the putative settlement class in Graff, the Court denied the collector’s request to stay the proceedings as moot, noting that it already granted the stay due to the DC Circuit appeal.

N.C. District Court Grants Stay of TCPA Lawsuit Pending DC Circuit Challenge to FCC Order

http://www.insidearm.com/daily/collection-laws-regulations/tcpa/n-c-district-court-grants-stay-of-tcpa-lawsuit-pending-dc-circuit-challenge-to-fcc-order/

http://www.insidearm.com/feed

insideARM

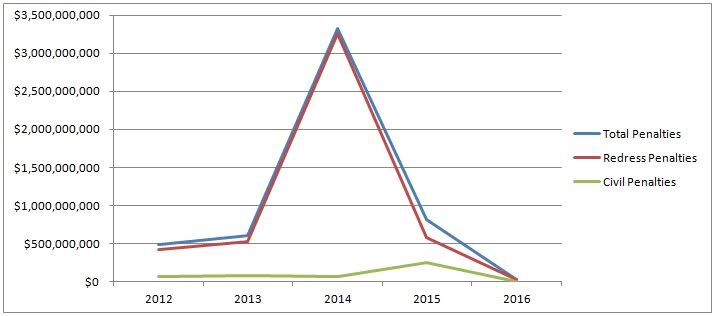

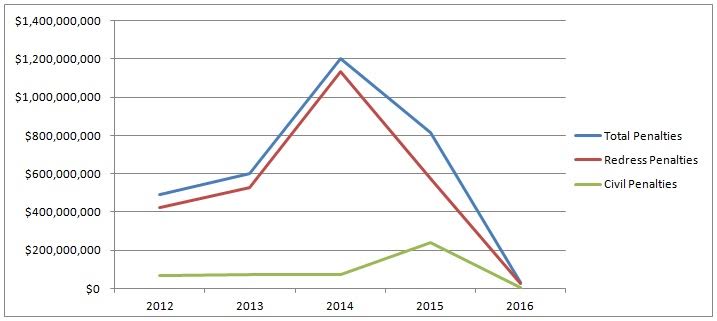

As you can see in the chart above, 2014 was a big year for the CFPB. The Bureau ended up issuing more than $3 billion in fines in 2014 alone, more than $2 billion of those penalties coming in

As you can see in the chart above, 2014 was a big year for the CFPB. The Bureau ended up issuing more than $3 billion in fines in 2014 alone, more than $2 billion of those penalties coming in  Types of Penalties

Types of Penalties