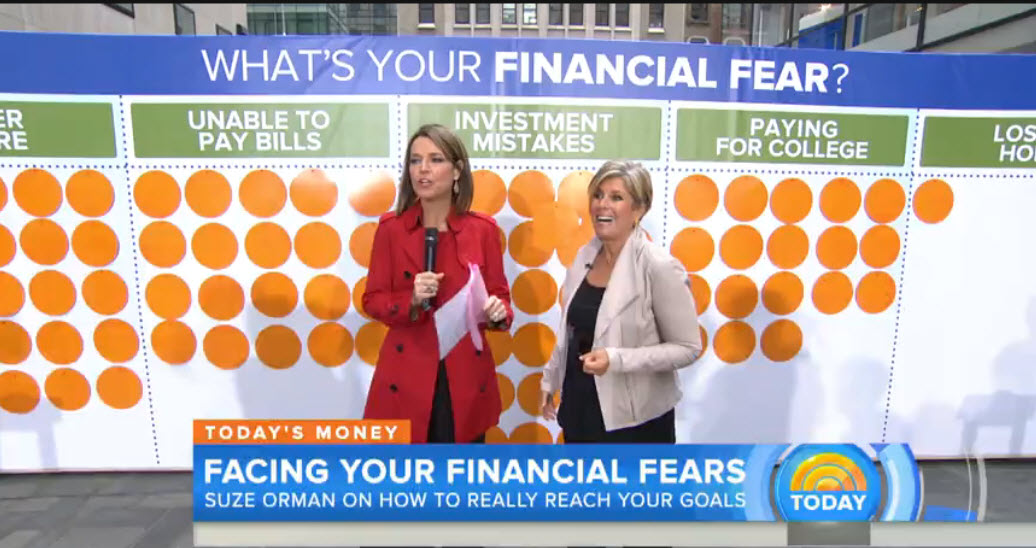

Earlier this week I was watching the Today Show (no comments, please), which included a segment with Suze Orman, the personal finance guru. She was there to promote her financial literacy course, and took a question from a young woman in the crowd. The woman said she is 25, recently graduated from college with $40,000 in student loan debt, and has just signed up for the income-based repayment program. She asked Suze whether this was the right thing to do. Without hesitation, Suze said unfortunately it was not the right thing to do. Her explanation was that the difference in what she should be paying (likely about $400/month) versus what she is probably now paying (likely about $150/month) gets shifted to the back end of the loan, and when the amount is forgiven years from now, she’s going to have a big tax bill.

I thought this was interesting, given how fervently the Department of Education has pushed this option. Was this the right advice? Do you agree? Click the image to watch the segment (the young woman’s question to Suze begins at 3:35).

Suze Orman on Today Advises Against Income-Based Student Loan Repayment Plans

http://www.insidearm.com/opinion/suze-orman-on-today-advises-against-income-based-student-loan-repayment-plans/

http://www.insidearm.com/feed

insideARM

Of prime interest to both groups, and where each spent considerable time, was in talking about the challenges entrenched collector behavior causes any agency and the frustrations around what, specifically, counts as a UDAAP: an Unfair, Deceptive, and Abusive Practice.

Of prime interest to both groups, and where each spent considerable time, was in talking about the challenges entrenched collector behavior causes any agency and the frustrations around what, specifically, counts as a UDAAP: an Unfair, Deceptive, and Abusive Practice.